Poliomyelitis is an acute infectious disease of viral origin and manifests itself as severe disturbances in the functioning of the nervous system as a result of damage to the cell bodies of neurons and unmyelinated axons of the spinal cord. The virus is spread throughout the globe. It is transmitted through nutritional (less often aerogenic) routes and often causes a pathological condition when, against the background of general inflammatory symptoms, paresis, paralysis, focal lesions of the head of the central nervous system and atrophy of the muscles of the extremities occur.

Unfortunately, there is no etiotropic therapy against poliovirus. The only proven way to prevent the most severe consequences of the disease is vaccination against polio, which allows you to form lasting immunity to the disease, that is, to protect the body from different strains of the virus that spread freely among members of the human population.

What is OPV vaccination?

OPV is an anti-polio vaccine for oral use, which contains live pathogen viruses. This immune drug is instilled onto the tongue of infants and onto the surface of the palatine tonsils of early preschool children. Once polioviruses enter the body, they enter the blood and with it the intestines, where the production of immune complexes that protect against the disease occurs. As of today, only one oral polio vaccine is approved in Russia, produced by the Federal State Unitary Enterprise “PIPVE named after M.P. Chumakov RAMS”, Russian Federation, Moscow region.

The vaccine includes three types of attenuated polioviruses that can completely cover the likelihood of infection with wild strains. In addition, the vaccine contains the antibacterial component kanamycin, which prevents the proliferation of bacteria in the nutrient medium.

In addition to OPV, the domestic vaccination calendar also includes IPV vaccination. Inactivated polio vaccine (IPV) contains killed viruses. It is administered by intramuscular or subcutaneous injection and does not promote the synthesis of antibodies on the surface of the intestinal mucous membranes. The risk of contracting a post-vaccination disease is zero.

What is required from Kazakhstani employers?

In order not to violate current legislation and not receive fines for late transfer of OPV, Kazakh employers need to promptly:

- compile lists of workers who are citizens of Russia, Kyrgyzstan, Armenia or Belarus, but do not have a residence permit in Kazakhstan (take into account both employment contracts and civil service agreements);

- calculate and transfer OPV from the income of such employees to the UAPF, starting in January 2021.

Let us remind you that the CPV rate is 10% of the taxable object (income), but the taxable income for calculating the CPV cannot exceed 50 minimum wages.

At the same time, a foreign employee, a citizen of the EAEU member countries, is not required to specifically contact the UAPF to conclude a pension agreement. As soon as the employer makes the first contribution for him, an individual pension account in the UAPF will be opened for the employee automatically. There is no need to submit a separate application.

Highlights of the instructions for use

According to the instructions, the vaccine is indicated for children aged 3 months to 14 years. It is an important part of routine immunization of the child population. In areas where there are frequent outbreaks of the disease, local authorities may decide on the advisability of administering an oral solution to a child immediately after birth, that is, in maternity hospitals. Vaccination is indicated for the following categories of adults:

- travelers and tourists, as well as diplomats who frequently visit countries with high incidence rates;

- virology laboratory workers;

- medical personnel who from time to time come into contact with people sick with polio.

OPV vaccination is a pink solution, enclosed in 5 ml bottles, each of which contains 25 doses of the vaccine. A single dose is four drops or 0.2 ml of liquid. It must be applied using a special pipette to the distal parts of the tongue or palatine tonsils. If a pipette is not available, it is recommended to use a syringe.

It is important that during the procedure, applying the solution does not provoke excessive salivation, regurgitation and vomiting, since a certain period of time is required for its absorption by the oral mucosa. If the weakened viruses were washed away by saliva or vomit, then immunity against polio will not be developed. If the drug was administered unsuccessfully, then it is necessary to repeat the attempt in the amount of one dose. If the baby burps for the second time, the third episode of vaccination is not repeated.

OPV combines well with various vaccines, will not interfere with the formation of an immune response to other diseases and will not affect the tolerability of other vaccine solutions. The exception is anti-tuberculosis suspension and oral drugs, so they are not combined with anti-polio vaccination.

Decoding of PFR in accounting

Payments of pensions and additional payments to pensions from the Pension Fund budget last year increased by 171.5 billion rubles and amounted to 7,339 billion rubles.

Social payments increased to 502.5 billion rubles. The provision of insurance pensions with received contributions exceeded 73%. All obligations to increase pensions and benefits were fulfilled on time and in full . By continuing to use our website, you consent to the processing of user data. More details (IP address; OS version; web browser version; device information (type, manufacturer, model); screen resolution and number of screen colors; Flash version; Silverlight version; availability of ad blocking software, availability of Cookies, availability of JavaScript ; OS and Browser language; time spent on the site; user actions on the site) in order to determine site traffic. OK

What are the contraindications and precautions?

Absolute contraindications to OPV are:

- the child has an immunodeficiency caused by cancer, severe forms of blood diseases or the human immunodeficiency virus;

- the occurrence of neurological complications during previous vaccination;

- development of a generalized allergic reaction to the first administration of a prophylactic suspension in the form of anaphylactic shock or angioedema;

- a situation when the child’s surroundings include people with severe immune system deficiency or pregnant females.

If immunization is necessary for children with diseases of the digestive tract, vaccinations should be given only in the presence of a doctor, after a detailed examination. The polio vaccine should not be given to children with fever or other symptoms of respiratory infections. In this scenario, vaccination should be postponed until the baby achieves complete remission and his immune function is restored.

As is known, live polioviruses multiply quite actively in the human body, therefore, after OPV, a vaccinated child can easily infect children without vaccine immunity. In order to prevent an outbreak of viral pathology, it is necessary to adhere to certain rules:

- replace live suspension with IPV for children who live with unvaccinated infants;

- temporarily (for 2-4 weeks) isolate children without immunity or who are exempt from vaccination from groups during the period of mass immunization;

- do not administer the attenuated vaccine to patients at tuberculosis dispensaries, as well as to residents of closed orphanages, boarding schools, and orphanages (it is recommended to replace it with IPV).

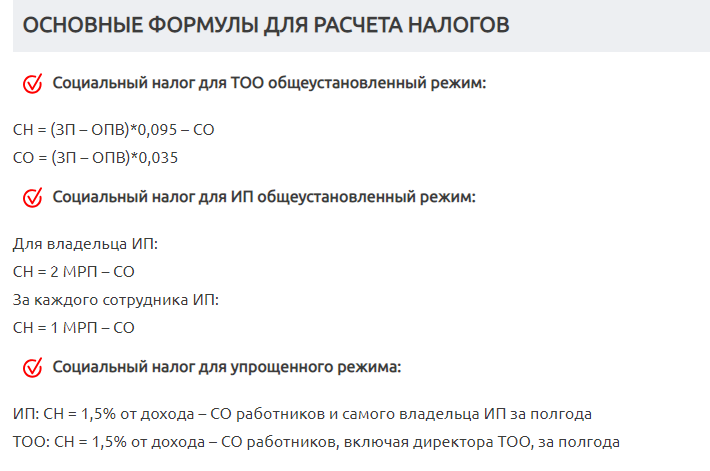

Tax rates in 2021 for SN

According to the changes of the current year, starting from January and up to 01/01/25, the tax rate will be equal to 9.5%. From 01/01/25 it will be increased to 11%. This requirement does not apply to individual entrepreneurs who work under the SNR. This category is calculated with the state using a separate formula.

Tax payers who are not legal entities make tax calculations of 1 MCI (monthly calculation index) for each employee and 2 MCI for themselves.

In the event that an individual entrepreneur did not receive income during the reporting period, he is exempt from the need to pay social tax. The same applies to taxpayers who have suspended reporting to the tax authorities.

Formulas for calculating taxes

Other tax rates for SN

As noted above, the 9.5% rate is not provided for all economic entities of the Republic of Kazakhstan. And also the following rates apply:

- 4,5%;

- 6,5%;

- 20% of the MCI.

4.5% is paid by specialized organizations that employ people with disabilities who have lost sight, hearing, speech or have disorders in the musculoskeletal system. This category of enterprises is determined by the Tax Code of the Republic of Kazakhstan, Article 135, paragraph 3 (download here).

6.5% must be transferred to the state treasury by legal entities engaged in agricultural activities and fishing. This category is also highlighted in the country's Tax Code in Article 147, paragraph 2 (download here).

Articles 358 (P.4) and 445 () refer to taxpayers who are obliged to pay 20% of the MCI. These are individual entrepreneurs (peasant and farm enterprises) who use SNR. Deductions are made for each employee of the farm, for the citizen who heads it and adult members of his family living with him.

The deadlines for submitting reports and the deadlines for transfers correspond to the deadlines provided for all social tax payers.

Are there any complications?

The most dangerous complication of immunization against polio is the vaccine-associated form of the disease. In this case, the virus takes on a type that easily paralyzes nerve cells and leads to reactive paralysis of the limbs. This adverse reaction to vaccination is extremely rare, occurring approximately once in 700 thousand cases.

The post-vaccination effect in the form of vaccine-associated polio occurs in most clinical cases after the first vaccination and very rarely after the second procedure. The peak of its manifestations occurs 6-14 days after the injection. Due to the increased risks of complications, the first two injections are given to infants using an inactivated vaccine, which does not provoke the development of pathological symptoms, but contributes to the formation of the necessary protection against the virus.

What is the RSV-1 form (abbreviation decoding)

The formation of RSV-1 is not so simple. It is for this reason that a large number of different specialized resources have appeared on the Internet, allowing you to use various programs to check whether the form has been filled out correctly.

But even if the document is not submitted through a special system created for the circulation of important documents between government agencies and enterprises, the submitter is required to submit to the relevant authorities not only two printed paper copies of the RSV-1, but also an electronic document on a flash card.

Timing of immunization

According to the national vaccination calendar, a child should be vaccinated within the following periods:

- The first IPV vaccine is given at 3 months;

- the second IPV is administered to babies at 4.5 months;

- at six months it is necessary to vaccinate for the first time with OPV;

- at 1.5 years - the first revaccination with OPV;

- at 20 months – repeated revaccination with a solution containing attenuated pathogens;

- The last injection is at 14 years old.

If the vaccination schedule is disrupted, this is not a reason to refuse subsequent vaccination. In this case, the doctor draws up an individual immunization plan, compliance with which will help achieve the desired effect and form reliable protection against polio. The minimum recommended interval between vaccinations should be at least 45 days. If desired, parents can immunize exclusively with an inactivated drug, naturally purchased with their own money.

The social tax rate is 9.5% according to Art. 485 Tax Code of the Republic of Kazakhstan.

At the same time, according to Article 486 of the Tax Code of the Republic of Kazakhstan, the amount of social tax payable to the budget is determined as the difference between the calculated social tax and the amount of social contributions calculated in accordance with the Law of the Republic of Kazakhstan “On Compulsory Social Insurance”.

If the amount of calculated social contributions to the State Social Insurance Fund exceeds the amount of calculated social tax or their amounts are equal, the amount of social tax payable to the budget is considered equal to zero.

It should be noted that mandatory pension contributions are not subject to social tax and should not be taken into account when calculating it.

If the object of taxation of SN for a calendar month amounts to an amount from one tenge to the minimum wage (42,500 tenge for 2021), established by the law on the republican budget and effective on the first day of this calendar month, then the object of taxation is determined based on such minimum salary amount.

Social tax = (accrued income - OPV 10%) * 9.5% - CO 3.5%.

More details about the calculation of Social Tax are indicated in Articles 482 – 489 of the Tax Code of the Republic of Kazakhstan.

Preparing for vaccination

Anti-polio immunization of children is carried out only after special training. It includes a number of activities, the main goal of which is to prevent the development of post-vaccination complications in children and their close circle. So, preparation begins with a medical examination of a small patient, determining his state of health, ruling out the presence of viral diseases, and the like. An important point is to assess the likelihood of infection of vulnerable members of the child’s family, including pregnant women, infants, and people with immunodeficiencies.

To avoid problems with the absorption of the vaccine fluid, the patient is prohibited from feeding and drinking for 1-1.5 hours before the procedure and a similar time period after it.

How to determine from what period to pay OPV or OPPV?

The agreement came into force on 01/01/2021. If, as of 01/01/2021, the employer has valid employment contracts or GPC agreements with foreign employees without a residence permit, citizens of the EAEU countries, he is obliged to begin withholding and transferring contributions from the employee’s income received for January 2021

Contributions must be transferred within the same time frame as for employees who are citizens of the Republic of Kazakhstan (by the 25th day of the month following the month of receipt of income). For income for January 2021, contributions must be transferred by 02/25/2021.

For violation of obligations to transfer OPV, the employer bears administrative responsibility (Article 91 of the Code of Administrative Offenses of the Republic of Kazakhstan):

- in case of a primary violation - a warning;

- in case of repeated violation, a fine of 20% of the amount of untransferred pension contributions.

If a foreigner employee from the EAEU entered into an employment contract (or GPC contract) during 2021, then the CPV must begin to be transferred from the month the contract was concluded. Thus, having concluded an agreement on 02/04/2021, it will be necessary to transfer OPV by 03/25/2021.

Side effects of immunization

As a result of clinical studies, doctors were able to confirm that children usually tolerate immunization that prevents polio. Therefore, on the day of vaccination, you can take a walk with your child, take water treatments and do other things according to your daily routine.

Side effects of vaccination are rare and most often take the following form:

- unexpressed digestive disorders, in particular, unformed stools, frequent urge to go to the toilet for 1-3 days;

- rashes of allergic origin that go away on their own without additional drug intervention;

- temporary nausea (possibly one-time vomiting without disturbing the general condition of the baby).

An increase in body temperature is not typical for the post-vaccination period. Therefore, the appearance of such symptoms should be associated with other causative factors. Do I need to be vaccinated against polio infection? Naturally, pediatricians insist on immunization of all children who have no contraindications to the procedure, but the last word should always remain with the parents of the little tomboy. When making a final decision, it should be taken into account that vaccinating children around the world has made it possible to minimize episodes of such a dangerous disease as polio, and has made it possible to prevent outbreaks of epidemics in different parts of our planet.

Should the bases for calculating OPV and CO IP for themselves be the same?

No, they shouldn't. The laws provide different upper limits for the amounts accepted as the base. This alone indicates that OPV and CO can be calculated from different amounts. The only constant is the requirement that the income accepted as the base does not exceed the taxable income of the individual entrepreneur.

At the same time, for his personal convenience, so as not to get confused in the calculations, the individual entrepreneur has the right, of course, to establish the same bases for calculating these two indicators. But this is his right, not his duty. You should focus only on the practical benefits of paying a larger or smaller amount of CO or OPV:

- does the individual entrepreneur plan to receive maternity benefits (then it makes sense to pay the employer above the minimum wage or even the maximum);

- perhaps retirement is just around the corner (then it makes sense to pay OPV to the maximum);

- Perhaps the individual entrepreneur does not count on payments from the State Social Insurance Fund and, in addition to the state pension, has provided himself with other sources of income in old age (then you can pay the minimum social security and social security benefits).

In the “Salary Calculator” service from Mybuh.kz, a special separate “tick” (“Separate CO base”) is provided for calculating CO. This will allow the individual entrepreneur to set as the basis for the CO for himself the amount that he considers necessary for himself (within the framework of legal restrictions).

Changes have been made to the Rules for the calculation and transfer of OPV

The Government of the Republic of Kazakhstan signed Decree of the Government of the Republic of Kazakhstan dated May 28, 2021 No. 332 On introducing amendments and additions to Decree of the Government of the Republic of Kazakhstan dated October 18, 2013 No. 1116 “On approval of the Rules and terms for calculation, deduction (accrual) and transfer of mandatory pension contributions, mandatory professional pension contributions to the unified accumulative pension fund and penalties on them"

The changes affected:

Objects of calculation of OPV

Income from which OPV is not withheld

Procedure for delivering notice of debt repayment

The changes apply to relationships arising from January 1, 2020.

In the Rules and terms of calculation, deduction (accrual) and transfer of mandatory pension contributions, mandatory professional pension contributions to the unified pension savings fund and penalties for them, approved by the specified resolution:

paragraph 5 is stated as follows:

"5. Mandatory pension contributions payable to the UAPF are calculated by applying the rate established by Article 25 of the Law to the object of calculation of mandatory pension contributions.

At the same time, the maximum total annual income accepted for calculating mandatory pension contributions should not exceed twelve amounts of fifty times the minimum wage established for the corresponding financial year by the law on the republican budget.

The objects of calculation of mandatory pension contributions are:

1) for legal entities - the monthly income of employees and individuals with whom civil contracts have been concluded, accepted for the calculation of mandatory pension contributions, which does not exceed fifty times the minimum wage established for the corresponding financial year by the law on the republican budget;

2) for persons engaged in private practice, as well as individual entrepreneurs using the labor of hired workers - the monthly income of the hired worker, accepted for the calculation of mandatory pension contributions, which does not exceed fifty times the minimum wage established by the law on the republican budget for the corresponding financial year;

3) for individuals receiving income under civil law contracts, the subject of which is the performance of work (provision of services), mandatory pension contributions payable to the unified accumulative pension fund are established in the amount of 10 percent of the income received, but not more than 10 percent of fifty times the minimum wage established for the corresponding financial year by the law on the republican budget;

4) for persons engaged in private practice, as well as individual entrepreneurs - income received.

In this case, the income received for persons engaged in private practice, as well as individual entrepreneurs for the purposes of calculating mandatory pension contributions is the amount determined by them independently within the limits established by paragraph 4 of Article 25 of the Law, but not more than the income determined for tax purposes in accordance with Tax Code.

In the absence of income, persons engaged in private practice, as well as individual entrepreneurs, have the right to pay mandatory pension contributions to the UAPF in their favor at the rate of 10 percent of the minimum wage established for the corresponding financial year by the law on the republican budget;

5) for a state corporation - monthly social payments in case of disability and (or) job loss in connection with caring for a child upon reaching the age of one year, as well as social payments in case of loss of income in connection with pregnancy, childbirth, adoption ( adoption) of a newborn child (children);

6) for the Ministry of Foreign Affairs of the Republic of Kazakhstan in terms of diplomatic service personnel working in foreign establishments of the Republic of Kazakhstan - 100 percent salary for positions equivalent to the personnel of the central office of the Ministry of Foreign Affairs of the Republic of Kazakhstan;

7) for an insurance organization - insurance payment as compensation for harm associated with loss of earnings (income);

for individuals receiving income under civil law contracts concluded with individuals who are not tax agents - income received under civil law contracts, the subject of which is the performance of work (rendering services);

for individuals receiving income under civil law contracts concluded with individuals who are not tax agents - income received under civil law contracts, the subject of which is the performance of work (rendering services);

9) for individuals who are payers of a single aggregate payment in accordance with Article 774 of the Tax Code, mandatory pension contributions in their favor, subject to payment to the unified accumulative pension fund, amount to 30 percent of 1 times the monthly calculation index - in cities of the republican and of regional significance, the capital and 0.5 times the monthly calculation indicator - in other localities. In this case, the size of the monthly calculation indicator established by the law on the republican budget and valid as of January 1 of the corresponding financial year is applied.”;

paragraph 6 is stated as follows:

"6. Mandatory pension contributions to the UAPF are not withheld from payments and income:

1) specified in paragraph 2 of Article 319 of the Tax Code, with the exception of persons specified in paragraph nine of subparagraph 31) of paragraph 2 of Article 319 of the Tax Code;

2) specified in Article 329, paragraph 1 of Article 330 of the Tax Code;

3) specified in paragraph 1 of Article 341 of the Tax Code, with the exception of those established by subparagraphs 12), 26), 27) and 50) of paragraph 1 of Article 341, as well as subparagraphs 42) and 43) of paragraph 1 of Article 341 of the Tax Code (in terms of lost earnings (income).

When calculating mandatory pension contributions, adjustments to the employee’s taxable income specified in subparagraph 49) of paragraph 1 of Article 341 of the Tax Code are not applied.

At the same time, mandatory pension contributions to the UAPF are not withheld from the income provided for in paragraph six of subparagraph 17) paragraph 1 of Article 341 of the Tax Code;

4) received in kind or in the form of material benefits by disabled people and other persons specified in subparagraph 2) of paragraph 1 of Article 346 of the Tax Code.

Of the social payments specified in subparagraph 26) of paragraph 1 of Article 341 of the Tax Code, mandatory pension contributions are withheld in accordance with the article of the Law of the Republic of Kazakhstan “On Compulsory Social Insurance.”;

paragraph 41 is worded as follows:

"41. The notice must be delivered to the agent personally against signature or in another way confirming the fact of sending and receipt. In this case, a notice sent in one of the following ways is considered delivered to the agent in the following cases:

1) by registered mail with notification - from the date the agent noted in the notification of the postal or other communication organization;

In this case, such notification must be delivered by postal or other communications organization no later than ten working days from the date of acceptance by the postal or other communications organization.

In the event of a return by a postal or other communications organization of the notice provided for in this paragraph, sent by the state revenue authorities to the agent by registered mail with notification, the date of delivery of such notice is the date of the tax examination with the involvement of attesting witnesses on the grounds and in the manner established by the Tax Code;

2) electronically:

from the date of delivery of the notification to the web application.

This method applies to an agent interacting with state revenue authorities electronically in accordance with the legislation of the Republic of Kazakhstan on electronic documents and electronic digital signatures;

from the date of delivery of the notification to the user’s personal account on the “electronic government” web portal.

This method applies to an agent registered on the “electronic government” web portal;

3) through the State Corporation “Government for Citizens” - from the date of its receipt in person.”;

clause 42-1 has been supplemented with the following content:

“42-1. In case of non-payment of arrears on compulsory pension contributions and compulsory professional pension contributions, lists of individuals in whose favor the arrears on compulsory pension contributions, compulsory professional pension contributions are being collected are submitted to the state revenue authority that sent the notification:

1) by an agent classified in accordance with the risk management system provided for by the tax legislation of the Republic of Kazakhstan as a high-risk category - within five working days from the date of delivery of the notification to him;

2) by an agent classified in accordance with the risk management system provided for by the tax legislation of the Republic of Kazakhstan, to the category of medium risk level - within fifteen working days from the date of delivery of the notification to him.”;

Clause 43 is worded as follows:

"43. Based on the lists submitted by the agent in accordance with paragraph 42-1 of these Rules, the state revenue authority collects the amounts of debt for compulsory pension contributions, compulsory professional pension contributions forcibly from the agents’ bank accounts no later than five working days from the date of receipt of the lists.

Collection of debt on compulsory pension contributions, compulsory professional pension contributions from bank accounts of agents is carried out on the basis of a collection order of the state revenue authority with the attachment of lists submitted by the agent.

If there is no or insufficient money in the bank account(s) to satisfy all the requirements for the client, the bank withdraws the client’s money in the order of priority established by the Civil Code of the Republic of Kazakhstan.

If there is no money in the agent’s bank account in national currency, debt collection on compulsory pension contributions and compulsory professional pension contributions is carried out from the agent’s bank accounts in foreign currency on the basis of collection orders issued in national currency by state revenue authorities.”

- Establish that paragraphs twenty-two, twenty-third and twenty-four of this resolution are valid until January 1, 2021.

- This resolution comes into effect upon the expiration of ten calendar days after the day of its first official publication and applies to relations arising from January 1, 2021.

Prime Minister

Republic of Kazakhstan A. Mamin